How a Mortgage Calculator Can Save You Thousands on Your Home Loan

When it comes to buying a home, one of the most important tools you can use is a mortgage calculator. This simple yet powerful tool can help you make informed decisions about your home loan, save money, and avoid financial pitfalls. In this article, we’ll explore how a mortgage calculator works, why it’s essential for homebuyers, and how it can save you thousands of dollars over the life of your loan.

What Is a Mortgage Calculator?

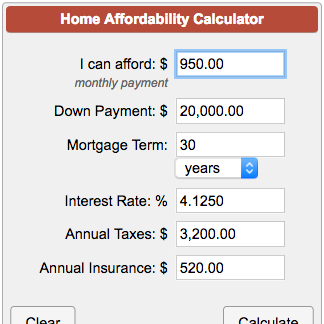

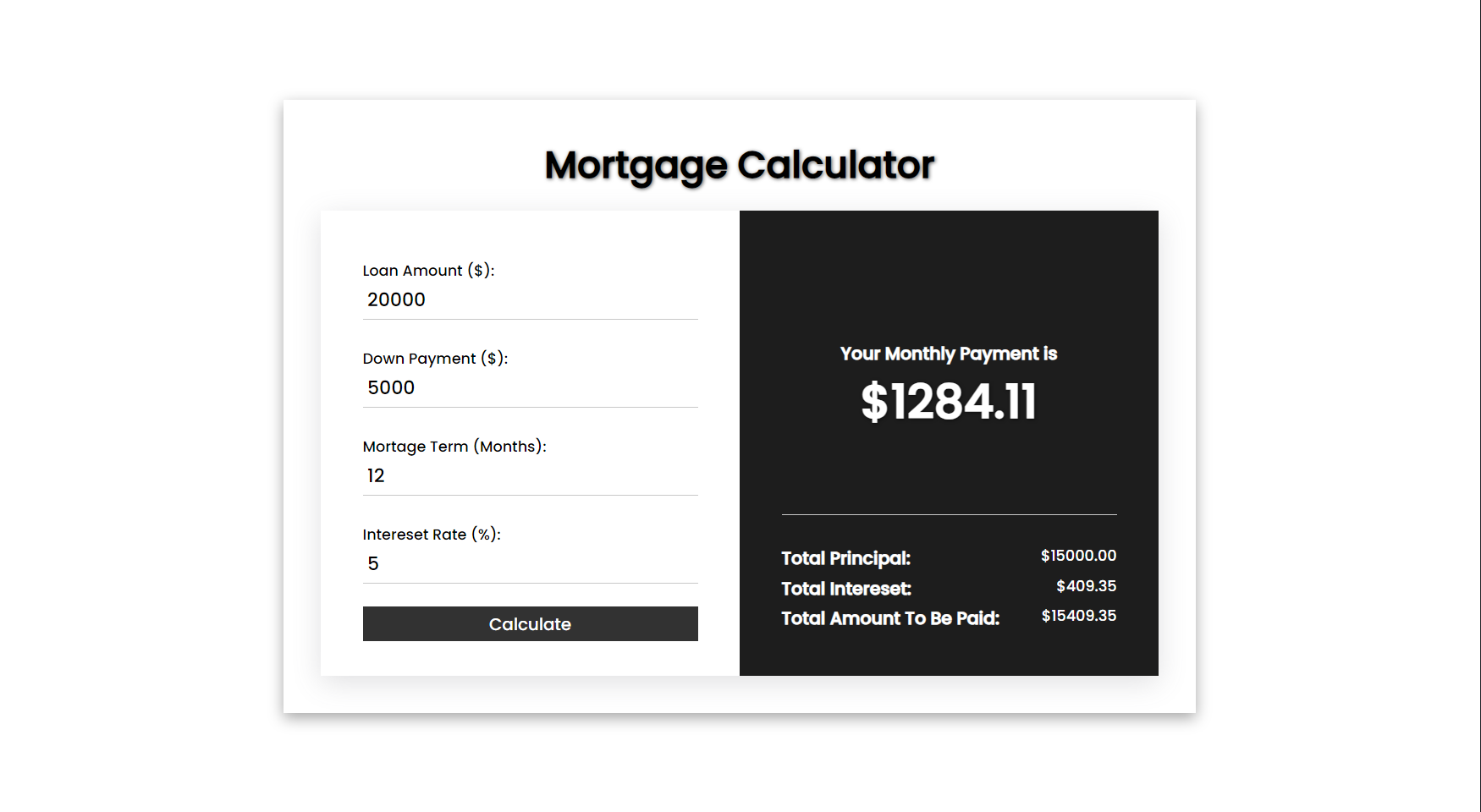

A mortgage calculator is an online tool that helps you estimate your monthly mortgage payments based on key factors such as:

- Loan amount

- Interest rate

- Loan term (length of the loan)

- Down payment

- Property taxes

- Homeowners insurance

By inputting these details into the calculator, you can get an accurate estimate of what your monthly payments will look like. Some advanced calculators also allow you to include additional costs like private mortgage insurance (PMI) or homeowners association (HOA) fees.

Why Should You Use a Mortgage Calculator?

Using a mortgage calculator is not just about crunching numbers; it’s about understanding your financial situation and making smarter decisions. Here are some reasons why every homebuyer should use one:

- Budget Planning

- A mortgage calculator helps you determine how much house you can afford.

- It ensures that your monthly payments fit within your budget without stretching your finances too thin.

- Comparison Shopping

- You can compare different loan options from various lenders.

- It allows you to see how changes in interest rates or loan terms affect your payments.

- Understanding Costs

- A good calculator breaks down the total cost of the loan, including interest paid over time.

- This transparency helps you understand the true cost of borrowing.

- Avoiding Surprises

- By factoring in property taxes and insurance, you get a more realistic picture of your monthly obligations.

- This prevents unexpected expenses from catching you off guard later.

How Does a Mortgage Calculator Work?

A mortgage calculator uses a standard formula to calculate monthly payments for fixed-rate loans:

(P × r × (1 + r)^n) ÷ ((1 + r)^n − 1)

Where:

- P = Principal loan amount

- r = Monthly interest rate (annual rate divided by 12)

- n = Total number of payments (loan term in years × 12)

While this formula might seem complex, the calculator does all the heavy lifting for you. All you need to do is input the required information.

Key Features of a Mortgage Calculator

Here are some features that make mortgage calculators incredibly useful:

- Loan Term Adjustment

- Allows you to see how different loan terms (e.g., 15 years vs. 30 years) impact your payments.

- Interest Rate Comparison

- Helps you understand how even small changes in interest rates affect overall costs.

- Down Payment Impact

- Shows how increasing or decreasing your down payment affects monthly payments and total interest paid.

- Amortization Schedule

- Provides a detailed breakdown of each payment, showing how much goes toward principal and interest over time.

- Extra Payments Option

- Lets you calculate savings from making extra payments toward the principal balance.

Ways a Mortgage Calculator Can Save You Money

Now let’s dive into specific ways this tool can help save thousands on your home loan:

1. Choosing the Right Loan Term

- A shorter loan term typically comes with higher monthly payments but lower overall interest costs.

- For example:

- A $200,000 loan at 4% interest over 30 years results in $143,739 in total interest.

- The same loan over 15 years results in only $66,288 in total interest—a savings of $77,451!

2. Comparing Interest Rates

- Even a small difference in interest rates can lead to significant savings.

- Example:

- A $250,000 loan at 4% has monthly payments of $1,193.

- At 3.75%, the payment drops to $1,158—saving $35 per month or $12,600 over 30 years!

3. Optimizing Your Down Payment

- Increasing your down payment reduces the amount borrowed and lowers PMI costs if applicable.

- Example:

- Putting down an extra $10,000 on a $300,000 home could save thousands in interest and eliminate PMI sooner.

4. Making Extra Payments

- Paying an additional $100 per month toward principal can shave years off your loan term and save tens of thousands in interest.

- Example:

- On a $200,000 loan at 4%, adding $100/month saves nearly $27,000 and shortens the term by five years!

5. Avoiding Over-Borrowing

- By using realistic inputs for taxes and insurance, calculators prevent buyers from taking on unaffordable loans.

Summary Table: Savings Scenarios

| Scenario | Potential Savings |

| Shorter Loan Term | Up to $77K |

| Lower Interest Rate | Up to $12K |

| Larger Down Payment | Varies |

| Extra Monthly Payments | Up to $27K |

Tips for Using a Mortgage Calculator Effectively

To maximize its benefits:

- Be Accurate: Use realistic estimates for taxes and insurance.

- Experiment: Test different scenarios by adjusting inputs like down payment or interest rate.

- Include All Costs: Don’t forget HOA fees or PMI if applicable.

- Plan Ahead: Factor in potential future expenses like maintenance or repairs.

Common Mistakes to Avoid

While mortgage calculators are helpful tools, there are some pitfalls to watch out for:

- Ignoring Additional Costs

- Many calculators focus only on principal and interest; make sure yours includes taxes and insurance.

- Using Unrealistic Interest Rates

- Advertised rates often assume excellent credit; use rates tailored to your credit score.

- Overestimating Income

- Be conservative when estimating income to avoid overstretching financially.

- Forgetting Closing Costs

- These upfront expenses aren’t included in most calculators but should be part of budgeting.

Advanced Features Worth Exploring

Some advanced calculators offer additional features that provide deeper insights:

- Biweekly Payment Options:

- Calculate savings from switching to biweekly payments instead of monthly ones.

- Refinancing Scenarios:

- Compare current loans with potential refinance options to evaluate savings opportunities.

- Rent vs Buy Analysis:

- Helps determine whether renting or buying makes more financial sense based on local market conditions.

Real-Life Examples

Let’s look at two real-life scenarios where using a mortgage calculator made all the difference:

Case Study #1: First-Time Buyer Saves Big with Extra Payments

John planned to buy his first home with a budgeted monthly payment of $1,500:

- Original Plan: Borrowed $250K at 4% for 30 years ($179K total interest).

- After Using Calculator: Added an extra $200/month toward principal—saved nearly $50K!

Case Study #2: Refinancing Decision Made Easy

Sarah had been paying her original mortgage at 5% but noticed rates dropped:

- Original Loan: Borrowed $300K at 5% ($279K total cost).

- After Refinancing: Switched to new rate at 3%—saved over $100K!

Conclusion

A mortgage calculator is not just another online tool—it’s an essential resource for anyone looking to buy or refinance their home responsibly while saving money along the way! By understanding its features and using it effectively during every stage—from planning through closing—you’ll gain confidence knowing exactly where every dollar goes while avoiding costly mistakes!