The Ultimate Guide to Mortgage Calculators: How They Work and Why You Need One

When it comes to buying a home or refinancing your current property, understanding the financial aspects of a mortgage is crucial. A mortgage calculator is one of the most valuable tools you can use during this process. It helps you estimate your monthly payments, understand how much house you can afford, and plan your finances effectively. In this guide, we’ll break down everything you need to know about mortgage calculators, how they work, and why they’re essential for anyone considering a home loan.

What Is a Mortgage Calculator?

A mortgage calculator is an online tool designed to help potential homebuyers or homeowners estimate their monthly mortgage payments based on several key factors. These calculators take into account variables such as:

- Loan amount

- Interest rate

- Loan term (e.g., 15 years, 30 years)

- Down payment

- Property taxes

- Homeowners insurance

- Private Mortgage Insurance (PMI), if applicable

By inputting these details into the calculator, you can get an estimate of what your monthly payments will look like. This information is invaluable when planning your budget and determining whether a particular home fits within your financial limits.

How Does a Mortgage Calculator Work?

Mortgage calculators use a mathematical formula to calculate your estimated monthly payment. The formula takes into account the principal loan amount, interest rate, and loan term to determine how much you’ll pay each month toward principal and interest.

Here’s the basic formula used by most mortgage calculators:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly payment

- P = Principal loan amount

- i = Monthly interest rate (annual rate divided by 12)

- n = Total number of payments (loan term in years multiplied by 12)

While this formula might seem complex at first glance, mortgage calculators simplify the process by doing all the math for you. All you need to do is enter the required inputs.

Key Components of Mortgage Calculations:

- Principal Loan Amount: This is the total amount borrowed from the lender after subtracting any down payment.

- Interest Rate: The percentage charged annually by the lender for borrowing money.

- Loan Term: The length of time over which you’ll repay the loan (e.g., 15 years or 30 years).

- Taxes and Insurance: Property taxes and homeowners insurance are often included in your monthly payment.

- PMI: If your down payment is less than 20%, private mortgage insurance may be required.

Why Do You Need a Mortgage Calculator?

Using a mortgage calculator offers several benefits that make it an essential tool for anyone considering buying or refinancing a home:

Helps You Budget Effectively:

- A mortgage calculator gives you an accurate estimate of your monthly payments so you can plan your budget accordingly.

- It helps ensure that you’re not taking on more debt than you can handle.

Determines Affordability:

- By entering different home prices into the calculator, you can see how much house you can afford based on your income and expenses.

Compares Loan Options:

- You can compare different loan terms (e.g., 15-year vs. 30-year) to see which option works best for your financial situation.

Shows Impact of Interest Rates:

- Even small changes in interest rates can significantly impact your monthly payments. A calculator lets you see how different rates affect affordability.

Plans for Additional Costs:

- Many calculators allow you to include property taxes, homeowners insurance, and PMI in your calculations so that you’re not caught off guard by additional costs.

Types of Mortgage Calculators

There are various types of mortgage calculators available online, each designed for specific purposes:

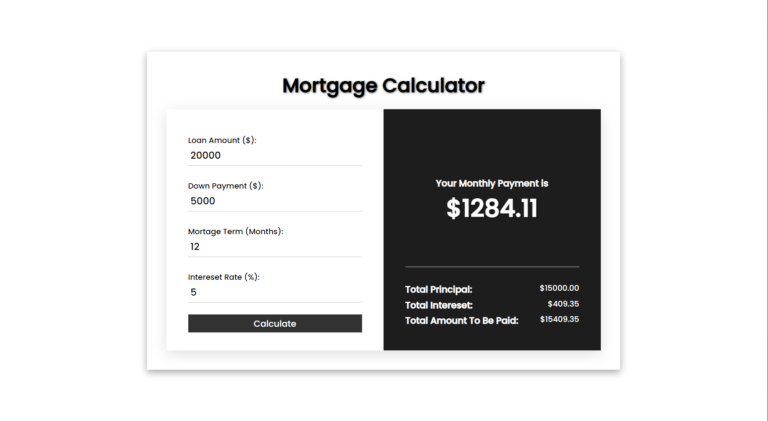

Basic Mortgage Payment Calculator:

This type calculates only the principal and interest portion of your monthly payment based on loan amount, interest rate, and term.

Full Payment Calculator:

Includes additional costs like property taxes, homeowners insurance, and PMI to give a more comprehensive estimate.

Refinance Calculator:

Helps homeowners determine whether refinancing their current mortgage would save them money by comparing their existing loan with new terms.

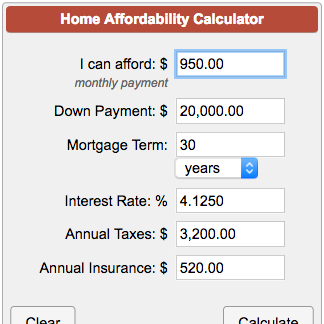

Affordability Calculator:

Estimates how much house you can afford based on income, debts, down payment size, and other factors.

Amortization Schedule Calculator:

Shows how much you’ll pay in principal versus interest over time and provides a detailed breakdown of each payment throughout the life of the loan.

How To Use a Mortgage Calculator Step-by-Step

Using a mortgage calculator is simple if you follow these steps:

- Enter Home Price:

- Input the price of the home you’re interested in purchasing or refinancing.

- Input Down Payment:

- Enter either the dollar amount or percentage you’re planning to put down upfront.

- Provide Loan Details:

- Include information such as loan term (e.g., 15 years or 30 years) and expected interest rate.

- Add Taxes & Insurance:

- If applicable, input estimated annual property taxes and homeowners insurance premiums.

- Include PMI (If Required):

- If you’re putting less than 20% down on a conventional loan, add PMI costs.

- Review Results:

- The calculator will display an estimated monthly payment along with a breakdown showing principal/interest versus taxes/insurance/PMI.

Benefits of Using Mortgage Calculators

Mortgage calculators provide numerous advantages that make them indispensable during any real estate transaction:

Saves Time:

Instead of manually calculating payments using complex formulas or spreadsheets, online tools provide instant results with just a few clicks.

Improves Decision-Making:

By comparing different scenarios side-by-side (e.g., varying down payments or interest rates), you’ll be better equipped to make informed decisions about loans or properties.

Reduces Stress:

Knowing what kind of financial commitment you’re getting into ahead-of-time eliminates surprises later-on during closing processes!

Common Mistakes When Using Mortgage Calculators

While these tools are incredibly helpful there are some common pitfalls users should avoid:

- Forgetting Additional Costs – Always include estimates for property taxes & homeowner’s insurances otherwise results won’t reflect true obligations!

- Overestimating Income Levels – Be realistic about earnings especially factoring-in other debts like car loans/student-loans etc!

- Ignoring Future Changes– Remember things like adjustable-rate mortgages could mean fluctuating-interest-rates overtime impacting affordability long-term!

Conclusion

In conclusion-mortgage-calculators offer powerful insights helping buyers/homeowners alike navigate complexities associated w/home-financing decisions! Whether estimating-affordability-comparing-loan-options-or-planning-budgets-these-tools-provide-clear-picture-of-financial-obligations-ahead!